The Central Asian countries have achieved significant socioeconomic progress since 2000; however, they need to overcome certain challenges to strengthen their economic growth and to make it more sustainable and less dependent on the export of commodities and receipt of remittances. Cooperative initiatives in the region have significant potential to foster economic growth, with infrastructure cooperation being especially important.

The Central Asian states have established themselves economically and have wide-ranging growth potential. Central Asia’s aggregate GDP totaled $397 billion in 2022 (see Figure A). Since 2000, this increased by a factor of 8.6. The region’s share of global GDP in purchasing power parity grew 1.8-fold. In most countries of the region, GDP per capita, PPP, increased threefold. The region’s population of 79 million has increased by a factor of 1.4 since 2000, forming a capacious sales market and an expanding pool of labor. Demographic data suggest that the workforce will continue to grow in the future. Population mobility has changed markedly, more than tripling between 2000 and 2019.

Figure A. The Region’s Achievements and Structural Changes

Note: pkm = person-kilometers

Source: EDB analysis based on national statistical agencies, IMF, UNCTAD, ADB, World Bank, Trade Map.

Increases in export revenues, migrant workers’ remittances, and foreign direct investment have fostered income growth and reduced poverty in Central Asia. The average annual economic growth rate for Central Asian countries has been 6.2 percent, which is faster than in many developing countries and more than twice as fast as the world as a whole. During this period, emerging countries and the world as a whole reported annual growth rates of 5.3 percent and 2.6 percent, respectively.

In 2022, the region’s foreign trade in goods totaled $211.2 billion and increased by a factor of 8.4. Mutual trade between the Central Asian countries is growing even faster than their total foreign trade. The share of mutual commodities trade in Central Asia’s total foreign trade went up from 6.4 percent in 2014 to 10.6 percent in 2022. Uzbekistan’s trading activity has given a significant boost to regional trade figures since 2017. The rate of development of regional trade affects investment cooperation. Priority areas of economic cooperation among the countries of the region are infrastructural development and industrial cooperation. Intra-regional cooperation will help to boost industrial production and improve the food security of the region.

In 2021, inward FDI stock in Central Asia totaled $211.4 billion. Since 2000, this figure has increased more than 17-fold. While FDI in the region is growing, its structure, both country- and sector-specific, reflects certain challenges. The lack of openness of some of the countries, their remoteness from major economic centers, and the fact that countries have no access to the world’s oceans, continue to affect international investors’ perception of the region. The ratio of FDI relative to GDP, excluding investment in the commodity sectors, is below the global average, indicating that the region is underinvested. In particular, about 70 percent of FDI stock in Kazakhstan, the region’s main recipient of foreign investment, is in the oil and gas sector. Moreover, China is actively increasing investments in the extractive assets of the Central Asian countries.

Sustainable development in Central Asia requires a balanced approach to attracting external funding – through strengthening and promoting good relations among the region’s countries and implementing the regional programs of international organizations and development banks. The Central Asian countries are implementing large-scale state programs and participating in major international initiatives, which open up unique opportunities to realize the region’s economic potential. There are a number of important programs offered by international institutions such as the World Bank, European Bank for Reconstruction and Development (EBRD), Asian Development Bank (ADB), Islamic Development Bank (IsDB), Eurasian Development Bank (EDB), the United Nations Economic and Social Commission for Asia and the Pacific (UNESCAP), the Economic Cooperation Organization (ECO), and the Shanghai Cooperation Organization (SCO). Funding will also require FDI in non-commodity sectors and use of the potential of domestic savings.

Despite progress, there are still problems that hinder the socioeconomic development of Central Asian countries. Commodity exports and migrant workers’ remittances continue to play a major role in the region’s economies. Other significant issues include the quality of the institutional environment, bottlenecks in regional transport networks, social issues, macroeconomic risks, and insufficient harmonization in regional trade and economic relations. The removal of structural development constraints remains a challenge for the Central Asian countries, too. These factors may become major risks for the future economic development of the countries.

If the landlocked Central Asian countries fail to create effective freight transit systems, they will fall behind countries that have access to the sea by 20 percent on average, and fail to be fully integrated into the world market. It is necessary to expand and improve the road and railway infrastructure, and to harmonize and simplify border-crossing procedures.

Another major risk is the increasing burden on water resources. This global challenge is particularly dangerous for the Central Asian region, as its countries are heavily dependent on agricultural production and vulnerable to the climate-related problems caused by drying up of bodies of water and melting glaciers.

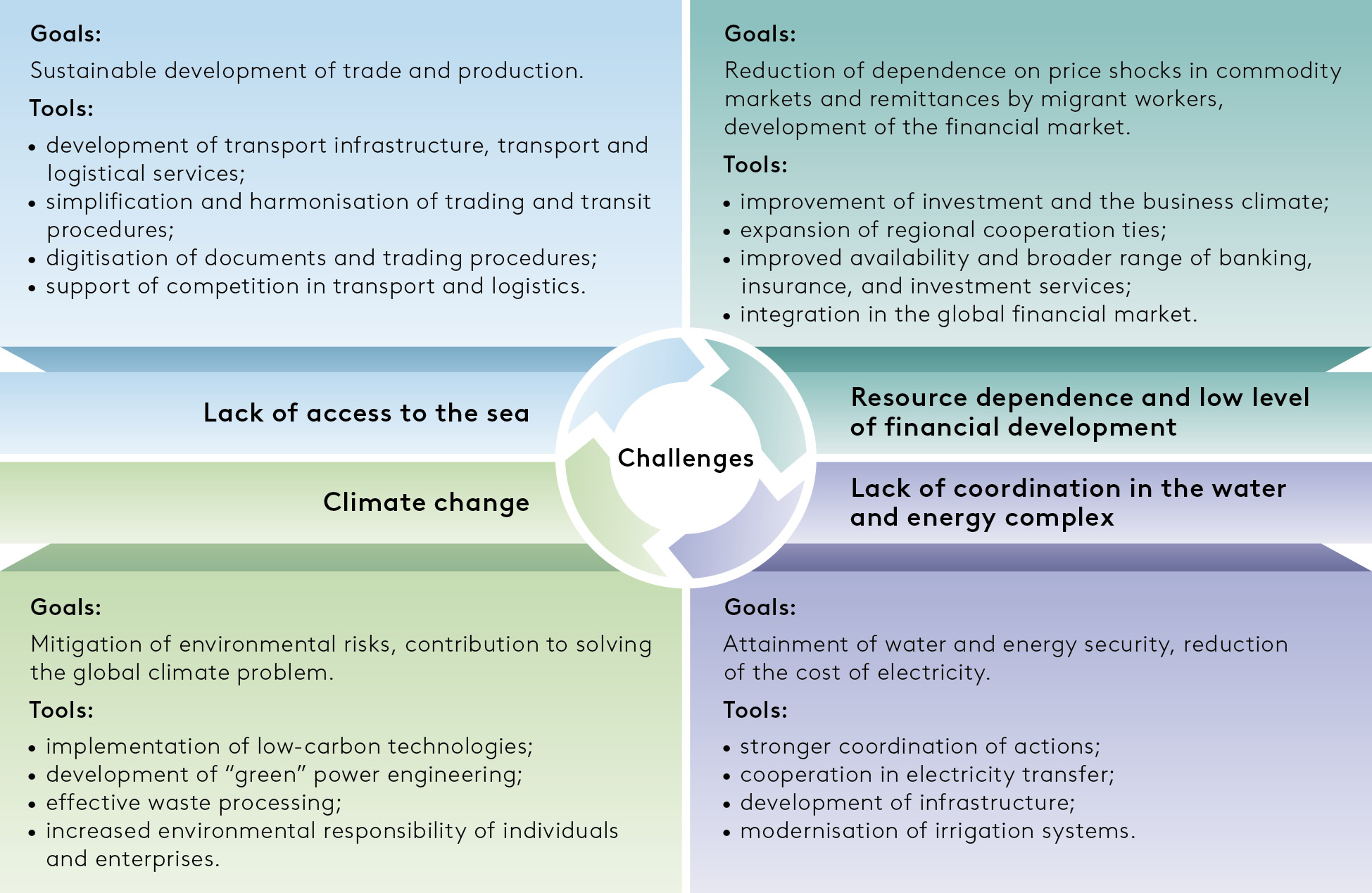

In our opinion, the region’s states need to overcome four key structural challenges: lack of access to the sea, low level of development of the financial sector, lack of coordination in management of the water and energy complex, and climate change (see Figure B).

Figure B. Structural Challenges and Mitigation Tools

Source: EDB.

Working together, the Central Asian countries will be better equipped to overcome structural development issues. Because of the increased burden on their energy systems due to active economic growth, and because of their connection through shared river basins, there is no alternative to cooperation among the Central Asian countries in the water and energy complex. Coordinated development of the water and energy complex, including green energy, also presents significant opportunities for growth. Joint actions to improve transport infrastructure and combat climate-related risks are equally important.

The inadequate level of cooperation in the water and energy complex inflicts economic damage from year to year. The unrealized benefits are estimated at 0.6 percent of the region’s aggregate GDP in agriculture, and 0.9 percent in the energy complex. The structure of the investment portfolio is far from optimal, as it fails to account for regional interests. Total investment proposals related to Central Asia’s water and energy complex are estimated at $52.8 billion, with the bulk of investment capital going to the generation segment. At the same time, water infrastructure facilities have exhausted their service lives and require upgrades and modernization. The Central Asian countries have abundant energy resources and a high renewable energy sources potential. Implementation of energy projects, including green power-engineering projects, will make it possible to improve the energy mix and, at a later stage, export electricity.

Transport infrastructure is developing dynamically and population mobility has increased. Efforts in that area have been hugely successful – the total length of railways and paved roads is growing. There are numerous new Caspian seaports, airports, transport and logistics centers, and border crossing points. Over the last several years, there has been a rapid increase in the volume of container transit using both the conventional route (China-Kazakhstan-Russia-EU) and the Trans-Caspian International Transport Route. New railway routes and container services will ensure more effective inclusion in global supply chains. The region’s countries have a historic opportunity to take advantage of their transit potential. North–South and West–East transport corridors and routes give the region a unique opportunity to turn from landlocked to land-linked countries and be revived as a transit crossroads.

Creation of their own financial sectors is a mandatory condition for sustainable development of the Central Asian countries. The population still prefers “conventional” forms of saving. The main tasks are to overcome lack of trust on the part of the population and to ensure diversified expansion of financial services. The regional financial markets should meet the challenge of harnessing intra-regional resources. Attraction of private savings alongside further development of financial services (banking, insurance, stock market) will contribute to the emergence of reliable sources of economic growth.

Central Asia is among the most vulnerable regions to climate change. Food supplies, water, and energy resources are particularly sensitive to climate challenges, and climate change poses the problem of conservation of biodiversity for the countries of the region. Environmental problems worsen living conditions, hinder economic development – especially in agriculture – and reduce the region’s appeal to investors and tourists. The region’s economies need green transformation and investment in low-carbon technologies and green projects.

Development of infrastructure presents the main structural challenges. Infrastructure projects are highly capital intensive. The Central Asian countries need to modernize and build their infrastructure. Geographical proximity encourages deeper infrastructural cooperation, and coordinated development of infrastructure creates synergetic benefits and helps save on cost. For example, the fact that West Africa has a shared power grid enables smaller countries to benefit from the economies of scale and risk-mitigating advantages of large power networks.

Eliminating bottlenecks in the infrastructural sectors (transport, the water and energy complex) will make it possible to improve economic productivity, expand trade, and promote economic partnership with neighboring countries, and increase product diversification of production and exports. The growing complementarity of the production structures will strengthen mutually beneficial cooperation among Central Asian countries and reduce their vulnerability to external shocks. Development of the institutional environment will enable an acceleration of structural economic transformation in the region.

Vulnerability to external factors can be reduced by fostering internal growth drivers. Transformation of the region largely depends on internal efforts, private investment, and large-scale multilateral programs. Central Asia can become a financially stable and dynamically developing region of Eurasia, employing effective regional cooperation mechanisms, and being actively involved in the operation of the value chains built by national businesses offering competitive goods and services to both domestic and foreign consumers.

Undoubtedly, Central Asia’s strategic role in Eurasia will increase, as well as its importance to neighboring countries and economic partners. The opportunities opening up before the Central Asian countries acquire special significance in the new geopolitical environment. Following a policy of openness, mutually beneficial cooperation, and coordination of efforts will enable the Central Asian countries to achieve a qualitative breakthrough in their development.